By: Richard_Mills

In 2001 and 2002 miners were producing gold for sub-$180 cash costs - the operational cost of the mine divided by the ounces of production. By 2005 cash costs had risen 45 percent to US$250. Data from GFMS shows world gold production costs for the first half of 2009 averaged $457/oz. Average cash costs in 2011 were US$657.

In 2001 and 2002 miners were producing gold for sub-$180 cash costs - the operational cost of the mine divided by the ounces of production. By 2005 cash costs had risen 45 percent to US$250. Data from GFMS shows world gold production costs for the first half of 2009 averaged $457/oz. Average cash costs in 2011 were US$657.

According to the Thomson Reuters GFMS?s Gold Survey 2012 global gold mine production was flat (output rose 0.1 percent to 1,366 metric tons) in the first half of 2012. The average grade of ore processed globally dropped 23 percent from 2005 through the end of last year and is forecast to decline another four percent in 2012.

The report also said the average cash cost across the gold mining industry for mining an ounce of gold is a record $727 per ounce. The average cash margin dropped to $872 an ounce in the second quarter from as much as $1,032 an ounce in last year?s third quarter

.

?Operating costs, the bullshine the industry is publishing as cash costs, are increasing, yields are declining and total expenditure has grown in line with the gold price.

Average operating/cash cost figures include only those costs directly associated with the production of the gold such as;

- Wages

- Cost of energy

- Raw materials such as steel, explosives etc

Thomson Reuters GFMS

But there?s more, a lot more to costs than most realize.

But there?s more, a lot more to costs than most realize.

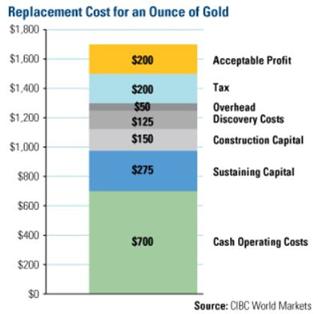

A complete breakdown of costs, an all-in cost figure, courtesy of CIBC, shows cash operating costs pegged at $700 an ounce, sustaining capital, construction capital, discovery costs and overhead at $600. Add in $200 for taxes and you get US$1500.00 as the replacement cost for an ounce of gold. Using the all-in figure provides a more accurate and definitive picture of actual mining cost and profit. Also, according to CIBC World Markets, the sustainable number gold miners need is $1,700/oz. As I write this gold is trading at $1726.00/oz.

It?s obvious that its very expensive to operate a gold mine and it?s not going to get any cheaper. The reasons behind flat-lining gold production, and record cash and all-in costs, are numerous:

- Production declines in mature mining areas

- Slower than expected ramp-ups of output

- Development time up

- The entire resource extraction industry suffers from a lack of skilled people

- Extreme weather

- Labor strikes

- Protests

Additional challenges include:

- Increasingly more remote and lacking in infrastructure projects

- Higher capex costs

- Increased resource nationalism

- Increased environmental regulation

- More complex metallurgy

- Lower cutoff grades

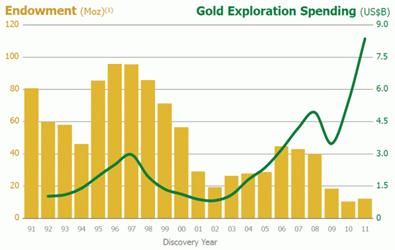

The biggest worry the industry has is that despite a significant investment in exploration (a record $8b in 2011) there?s a lack of discovery with few large high grade deposits being discovered.

?

Here?s some excellent insight from Brent Cook, explorationinsights.com.

?Major gold mining companies are facing a big problem. They are unable to find and develop enough ounces to keep up with demand, for the simple fact that economic gold deposits are extremely rare. Production shows a very simple trend: it rose until about 2000 and has fallen since then. This reduced production occurred even as the price of gold has increased nearly 400% in the past ten years. This incongruity tells us something fundamental: there?s a problem.

There are three main reasons why gold production increased up to 2000 despite declining gold prices.

- The first is the advent of new mining and processing technologies that made previously uneconomic low grade deposits economic. This was mostly a result of heap leach technology and bulk mining methods. Meaning, mining companies could now scrape up large areas of low grade mineralization and sprinkle a cheap solution of cyanide on the rock to recover the gold. This primarily worked on near surface oxidized deposits in relatively dry climates.

- The second is that vast regions of the world that had previously been closed for various reasons were opened up to exploration. These new areas include much of Latin America, Africa, and the former Soviet Union. I was part of that movement; we were able to walk onto obvious deposits with new eyes and rapidly drill out those resources. It also became markedly easier to get into these areas, so we were able to go deeper into the jungles and deserts.

- The third is that geologists had a whole slew of new exploration tools with which to scan the earth. These include satellite imagery, geophysics, and more sensitive chemical tools.

The net result was that new technologies kept old deposits going longer and made previously uneconomic ones viable, thereby ramping up production into the early 90?s. New deposits in previously unexplored and off-limits areas kept that production going until about 2000. All well and good but the industry is not finding as many new deposits as they need to in order to maintain current production levels. And, although we can expect incremental technological improvements in processing, mining, and exploration, there is nothing revolutionary on the horizon.

This is a worrisome slide for major gold producers?they are unable to sustain themselves. For the most part they are surviving via old deposits that are running out of ore and newer deposits that are quickly headed into the ?old? deposit category. Reserves from these aging deposits are not being replaced by new discoveries. Producers? problems are further exacerbated by rising exploration and development costs, plus the significant time it now takes to permit and finance a new deposit.?

Here?s Paul van Eeden (paulvaneeden.com) on reserve replacement, this was written in 2001:

?Worldwide gold production from mining is approximately 80 million ounces per year. A few years ago, a world-class gold discovery, which rarely occurs, would have been anything over a million ounces. Perhaps a few such deposits are discovered in a decade yet we mine the equivalent of 80 such deposits a year. Due to recent mergers and acquisition in the mining industry, the bar has been raised and the major mining companies now require deposits to be in excess of 5 million ounces before they become excited. Perhaps only one or two such discoveries are made in a decade. Anglogold mines over 6 million ounces of gold a year. Newmont mines roughly 4 million ounces of gold a year, Barrick 3, Harmony almost 3, Normandy 2, you get the picture. Each of these companies need to make a world-class discovery every year, and some of them need several, just to prevent the natural depletion of their mineral reserves from retiring the entire business. Note that mergers and acquisitions do not add any new resources to the mining industry, it merely changes the ownership of mines. The gold mining industry needs to discover 80 million ounces of gold every year just to prevent it from shrinking and it is highly unlikely that we will ever discover 80 million ounces in any given year, never mind do so on a continuous basis.?

Barclays Plc predicts global gold mine output may increase 0.7 percent in 2013, the slowest pace since 2008, while forecasting total physical supply may shrink 0.4 percent in 2014.

Gold miners have been able to survive rising costs because of rising gold prices ? if gold prices do not start going up marginal projects are not going to get funded and a whole lot of forecasted gold production is not going to come on stream.

Global gold demand in Q3 2012 was 1,084.6 tonnes (t), slightly above the five year quarterly average of 984.7t, according to the World Gold Council's Gold Demand Trends Report.

?Gold is beginning to re-establish itself as part of the fabric of the financial system. In the medium term, the quantitative easing initiatives in the West and the continuing growth story in the East, particularly in India and China, coupled with the seasonally strong quarter coming up in Asia, are excellent indicators for further growth in the gold market?it is clear from five year rising demand trends that gold's fundamental property as a vehicle for capital preservation continues to endure, as evidenced by this quarter's increase in global ETF investment, up 56% and continued purchasing by central banks, the ultimate long term investors.? Marcus Grubb, Managing Director, Investment at the World Gold Council

From Sy Harding, over at streetsmartreports.com, comes some important information on the state of the U.S. economy:

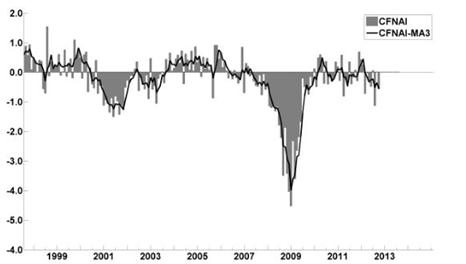

?The CFNAI is an index comprised of 85 established economic indicators and trends drawn from all areas of the economy. It was first compiled in 1967 and has a remarkable record for identifying early on when the economy has entered a recession.

The numbers are reported monthly. A positive level for the index indicates the economy is growing, while a negative number indicates the economy is slowing.

The index has been of concern for a while. The monthly reading of the index was in negative territory for five consecutive months before improving to the flat-line at 0.0 in September.

Unfortunately, that improvement lasted only one month. The report this week shows a sizable drop to -0.56 in October.

More ominously, it?s more important 3-month moving average also dropped to -0.56 in October from -0.36 in September. It was its 8th straight month of negative readings, and getting ominously close to the -0.70 level the Fed considers ?an increasing likelihood that a recession has begun.? It is the solid line in the Fed?s chart.

The index has only dropped beneath the recession warning level of -0.7 eight times since 1967. That was in 1970, 1974, 1980, 1981, 1989, 1990, 2001, and 2008. Each time the economy was indeed in a serious slowdown, usually a recession, and seven of those eight times the stock market was already in a bear market or soon rolled over into one. The most recent occasions were in 2001 and 2008, certainly not pleasant memories for the country.

The financial media and investors don?t pay much attention to the CFNAI, and most of the time it is not of much importance.

But with the 3-month moving average in negative territory for 8 straight months, and now at -0.56, so perilously close to -0.70, it should have everyone?s attention.?

From Axel Merk, over at merkinvestments.com, comes three key reasons to support an investment in gold:

- A form of protection against inflation

- Safe haven investment

- Minimize downside deviations in the value of an overall portfolio, reduce overall volatility, and enhance returns

?Over recent years, gold has performed remarkably well relative to other asset classes, in terms of both absolute performance and risk-adjusted performance. Over the preceding 10 years, an investment in gold would have significantly outperformed a corresponding investment in the S&P 500 Index or U.S. bonds, not to mention international and emerging market equities. Over the past 10 years, gold outperformed U.S. equities by over three times.

On a risk-adjusted basis, gold has produced superior returns, as measured by the Sharpe ratio. Over the 10-year period ended September 30, 2012, gold?s performance generated a Sharpe ratio of 0.85. In comparison, the S&P 500 Index generated a Sharpe ratio of just 0.30, as did international equities.

Gold?s Sharpe ratio was nearly as high over the five year period, as it was over the 10-year period ended September 30, 2012, while comparable equity indices produced negative Sharpe ratios. In fact, over each time period analyzed, gold outperformed domestic and international equities on a risk-adjusted basis.?

?

?

merkinvestments.com

?The disadvantage of fiat money [.i.e. non-convertible money], relative to commodity money, rests precisely in the fact that its scarcity, being thus contrived, is also contingent. A matter of deliberate policy only, it is subject to adjustment at the will of the monetary authorities or, if those authorities are bound by a monetary rule, at that of the legislature. Consequently, although a fiat money can be managed so as to not only preserve its purchasing power over time, but also so as to achieve the greatest possible degree of overall macroeconomic stability, there is no guarantee that it will be so managed, and market forces themselves offer no effective check against its arbitrary mismanagement.? economist George Selgin

Conclusion

It?s very clear that over the last decade gold has been a very good investment, and will continue to be so for the foreseeable future, but there is one asset class that will do even better then bullion, a lot better.

As mentioned previously, producers are not able to replace their reserves because there?s a lack of discovery, few large high grade deposits are being discovered and most of those that have been discovered aren?t owned by producers ?

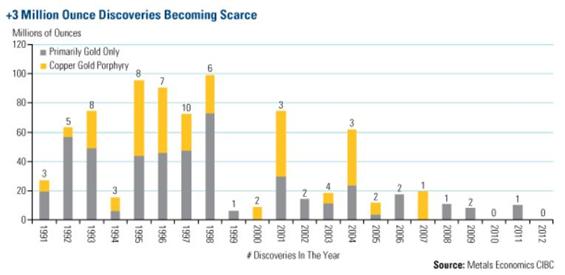

?Today, the major producers and their majority-owned subsidiaries hold 39 percent of the reserves and resources in the 99 significant discoveries made in the past 15 years.? Metals Economics Group (MEG)

Only 39 percent, so who owns the other 61 percent, who actually owns the worlds future gold supply?

A Junior exploration company?s place in the food chain is to acquire and explore properties. Their job is to make the discoveries that the mid-tiers and majors takeover and turn into mines. Junior exploration companies own the majority of the world?s future gold mines.

But the bottom line is, new exploration, despite a record amount of money being thrown at it, is not keeping up with reserve depletion. Juniors are not getting enough funding to do the necessary exploration to keep up - from June 2011 to June 2012 funding for juniors has dropped by $9b.

It?s time to be a stock picker, you need to find the quality management teams with money in the treasury, the ability to raise more and having the advanced projects that are well along the development path towards a mine. A mine that is going to be a long life, lowest quartile all-in cost producer. These companies are the world?s future gold producers and of course most will be in the sights of mid-tier and major producers for takeover candidates as reserve replacement targets.

I?ve got several precious metal juniors that fit that very specific bill on my radar screen, do you have any on yours?

If not, maybe they should be.

By Richard (Rick) Mills

www.aheadoftheherd.com

rick@aheadoftheherd.com

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including:

Wall Street Journal, Market Oracle, SafeHaven , USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright ? 2012 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

? 2005-2012 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Source: http://www.marketoracle.co.uk/Article37821.html

moonrise kingdom coachella lineup coachella 2012 lineup school delays joran van der sloot honey badger critics choice awards 2012

No comments:

Post a Comment